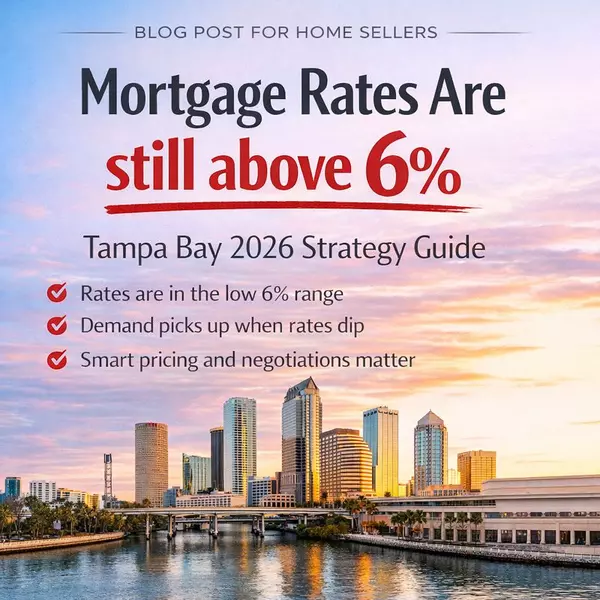

Mortgage Rates Are Still Above 6%: What Tampa Bay Home Sellers Should Know in 2026

Updated: January 14, 2026

Mortgage rates are still generally above 6%, but the bigger story for sellers is how buyers are adapting—and how the market is responding. National benchmarks in early January 2026 show the 30-year fixed mortgage in the low-6% range, depending on the survey. Freddie Mac reported 6.16% (week ending Jan 8, 2026), the MBA reported 6.25% (week ending Jan 7, 2026), and Bankrate showed a 6.20% national average APR on Jan 14, 2026. Rates change daily and vary by borrower.

The quick takeaway for Tampa Bay sellers

- 6%+ rates don’t stop sales—they change what buyers prioritize (monthly payment and total “cost to own”).

- Small rate dips can bring buyers off the fence, so being “market-ready” early can matter.

- Strategy wins in this environment: pricing accuracy + presentation + smart negotiation levers.

Where mortgage rates are right now (and why it matters)

In early January 2026, national averages have hovered around the low-6% range. That’s still higher than many buyers were used to years ago, but it’s also meaningfully lower than the ~7% range seen at points in 2025. Freddie Mac’s weekly survey shows the 30-year fixed rate was 6.16% as of Jan 8, 2026, compared with 6.93% one year earlier—an improvement that can expand buyer affordability at the margins.

In practice, buyers often shop by monthly payment. When rates fall even slightly, buyers who were “close” on affordability can re-enter the market—especially for homes that are well-priced and easy to say yes to.

What I’m seeing nationally: demand improves when rates ease

Nationally, late-2025 and early-2026 data has pointed to improving momentum as rates eased and sales activity picked up. For example, U.S. existing home sales rose in December 2025, with analysts noting that lower mortgage rates helped support demand. Inventory was still relatively tight, which is one reason well-prepared, well-positioned listings can stand out.

Translation for sellers: you don’t need “perfect” rates—you need a plan that matches today’s buyer behavior.

What this means specifically for Tampa Bay sellers

Tampa Bay is not one market—it’s many micro-markets. But recent Tampa trends show homes taking longer to sell than last year. Redfin reported that in December 2025, Tampa homes averaged about 66 days on market (vs. 47 days the year prior). Pinellas County averaged about 60 days (vs. 52 the year prior). These are broad indicators, not a prediction for your specific home—but they do reinforce the need for sharp pricing and strong presentation.

Seller advantage: When buyers are more selective, the homes that feel “easy” (clean, updated, documented, and priced correctly) tend to capture the best offers.

The 3 seller levers that matter most when rates are above 6%

1) Pricing precision (not optimism)

In a payment-sensitive market, “almost right” pricing can get punished with extra days on market—then bigger negotiation later. A pricing strategy built around recent comparable sales, current competition, and buyer psychology can create urgency instead of hesitation.

2) Presentation that removes objections

When buyers feel rate pressure, they often become more condition-conscious. A few high-ROI moves can help:

- Pre-list inspection (when appropriate) or proactive repair plan

- Fresh paint and lighting improvements

- Professional photography and a clean “first 8 seconds” visual impact

- Clear disclosures and docs ready (HOA/condo docs, permits, warranties, etc.)

3) Smart concessions (to protect your net)

This is where many sellers can improve outcomes without “giving away the house.” In some scenarios, a targeted concession (like a closing cost credit) can help a buyer’s monthly payment or cash-to-close more effectively than a small price cut. The right approach depends on your price point, your buyer pool, and current competition.

Note: Rate buydowns and loan structures must be modeled by a lender and vary by buyer qualification. This is general information, not financial advice.

If you’re considering selling in 2026, here’s a simple plan

- Define the goal: timeline, target net, and non-negotiables.

- Price with the market you have: today’s buyers, today’s competition.

- Choose your negotiation “menu” in advance: what you’ll fix, credit, or decline.

- Launch with strength: photos, marketing, and showing access that make it easy to view.

- Have a 21–30 day checkpoint: if activity is soft, adjust quickly and strategically.

FAQ: Mortgage rates above 6% and selling in Tampa Bay

Will 6%+ rates prevent my home from selling?

Not necessarily. Homes sell every day with 6%+ rates. The bigger factor is whether your home is priced and presented to match payment-conscious buyers.

Should I wait for rates to drop before listing?

Waiting can work for some sellers, but it can also mean more competition later if many homeowners list at the same time. A practical approach is to get “market-ready” so you can move when timing is right for you—especially when rates show short-term dips.

Are seller credits becoming more common?

In many markets, yes—because they can help buyers manage cash-to-close or monthly payment scenarios. The right strategy depends on your local competition and the type of buyer your home attracts.

How do I know the right price in today’s market?

A strong pricing plan looks at recent comparable sales, active competition, and the “why” behind buyer decisions (payment, condition, location fit, and friction). I also like to map out likely objections and solutions before launch.

Thinking about selling? I’ll build your “rate-impact” selling plan

If you’re considering a sale in Tampa Bay, I can put together a tailored plan for your property: pricing strategy, likely buyer objections, concession options (if needed), and a marketing approach designed to reduce friction and protect your net.

Text or call: 813-205-5430

Instagram: @shanevanderson

Website: shanevanderson.com

Disclaimer: This article is general information and not financial, legal, or tax advice. Mortgage rates vary daily and by borrower. Consult a qualified mortgage professional for scenarios.

Categories

- All Blogs (140)

- 345 Bayshore (3)

- 400 Central (2)

- Apollo Beach (24)

- Arbor Greene (7)

- Avila (39)

- Ballast Point (6)

- Bayshore Beautiful (6)

- Beach Park (34)

- Bel Mar Gardens (4)

- Belleair Beach (5)

- Brandon (11)

- Carrollwood (33)

- Channel District (12)

- Cheval (21)

- Clearwater (34)

- Clearwater Beach (14)

- Cordoba Ranch (6)

- Cory Lake Isles (5)

- Culbreath Isles (23)

- Davis Islands (43)

- Downtown St Petersburg (17)

- Downtown Tampa (48)

- Golfview (18)

- Grand Central at Kennedy (1)

- Gulf Beaches (5)

- Harbour Island (47)

- Home Buying (9)

- Home Improvement (1)

- Home Selling (23)

- Hotel ORA (1)

- Hunters Green (16)

- Hyde Park (37)

- Indian Rocks Beach (9)

- Ladera (8)

- Lakewood Ranch (9)

- lutz (40)

- Luxury Homes (6)

- Madeira Beach (23)

- Marina Pointe (23)

- Market Health Update (20)

- New Suburb Beautiful (3)

- New Tampa (12)

- Odessa (30)

- Old Northeast (3)

- ONE St. Petersburg (1)

- ONE Tampa (4)

- Palma Ceia (8)

- Parkland Estates (4)

- Pendry Tampa (7)

- Pinellas Condos (7)

- Plaza Harbour Island (4)

- Reviews (2)

- Ritz-Carlton Tampa (11)

- Riverview (27)

- Safety Harbor (4)

- Saltaire (1)

- Seminole Heights (26)

- Skypoint (5)

- Snell Isle (22)

- South Tampa (78)

- St Pete Beach (28)

- St Petersburg (50)

- Sunset Park (30)

- Tampa (78)

- Tampa Bay New Construction (2)

- Tampa Bay Real Estate (41)

- Tampa Bay Waterfront (3)

- Tampa Condos (12)

- Tampa Edition (9)

- Tampa Palms (22)

- The Nolen (3)

- The Place Channelside (1)

- Tierra Verde (21)

- Towers of Channelside (2)

- Treasure Island (4)

- Venetian Isles (21)

- Viceroy Clearwater Beach (2)

- Virginia Park (12)

- Waldorf Astoria St Petersburg (4)

- Water Street (22)

- Waterleaf (4)

- Westchase (33)

- Westshore Marina District (26)

- Westshore Yacht Club (6)

- Ybor (8)

Recent Posts